Today, we’re here to answer your Health Insurance Exchange FAQs, including an overview of plans and the key terms you need to know when shopping for health insurance.

Health Insurance Exchange FAQs: Enrollment

Open enrollment for the health insurance exchange is from November 1 to January 31st. So, for 2017 coverage you will need to make a choice between November 1, 2016 and the end of January of 2017. This is the ONLY time you can enroll, unless you qualify for a Special Enrollment Period (SEP). See our prior post for more on 2017 open enrollment and when you might qualify for a SEP (or to get insurance other ways).

Mandate: Under the Affordable Care Act (ACA), individuals (with a few exceptions) must have health insurance that meets minimum standards or face a penalty. Here is a good review of the penalty (and a calculator) that also lists the exceptions to the individual mandate.

Health Insurance Exchange FAQs: Coverage Levels and Costs

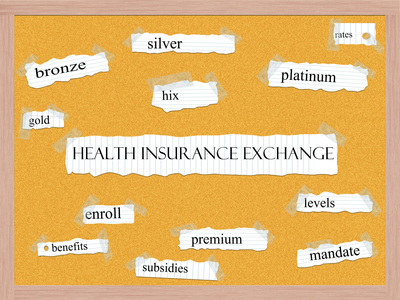

No matter what level of plan you choose (or which carrier), plans must cover the required essential health benefits. The four coverage levels are based on the amount you can expect the plan to pay versus your expenses (the actuarial value, i.e the average). Higher level plans (gold and platinum) mean you will pay less out-of-pocket for things like deductibles–the amount you pay 1st before coverage kicks in, copays– a fixed amount you pay for services, and coinsurance-share of cost for covered services). However, premiums (the monthly amount you pay to have the coverage) on these plans would typically be higher. Here are the approximate amounts covered by the plan levels (their actuarial values):

Bronze = 60%

Silver = 70%

Gold = 80%

Platinum = 90%

If your income falls between 100-250% of the federal poverty level, you may be eligible for a Cost-Sharing Reduction subsidy, which can help lower your deductibles, copays, and coinsurance.

Many people (100-400% of poverty level) will qualify for Advanced Premium Tax Credits, a subsidy to help lower your premiums.

You must apply for these subsidies; they are not automatically applied.

Premiums are based on age, where you live, whether or not you’re a smoker, total # enrolling (i.e. spouse or children), and the insurance company you choose. Within the cost structure noted above, the plan may set up the cost sharing in different ways (for example, one Gold plan may have a high deductible and lower copays/coinsurance while another may have a lower deductible and higher shared costs for covered services).

Finding the Best Plan

During open enrollment, visit healthcare.gov to check your eligibility, review plans and complete an application. Pinellas County also offers an Affordable Healthcare Navigator program to help you look for/enroll in a plan (and understand subsidies/financial help, find alternative options, guide you through appeals and exemptions, and more). You can also contact a local insurance broker for help finding options.

News/Updates

We hope this review of the health insurance exchange FAQs makes it easier for you to understand your options and all the terms being thrown around. Premiums are projected to rise by about 19% for Floridians who buy individual insurance in 2017. An estimated 1.53 million Floridians bought plans on the exchange this year (according to the Department of Health and Human Services) and most (about 93%) qualified for subsidies to make coverage more affordable. Florida has been lagging in rates of insured residents, but continued outreach is closing this gap.

Premiums, cost sharing, and plan availability (in different areas of the state) vary widely, so take the time to look at your options and don’t make assumptions about what might be out there for you.